News

Why Nigeria’s Cocoa Needs More Than Price Spikes

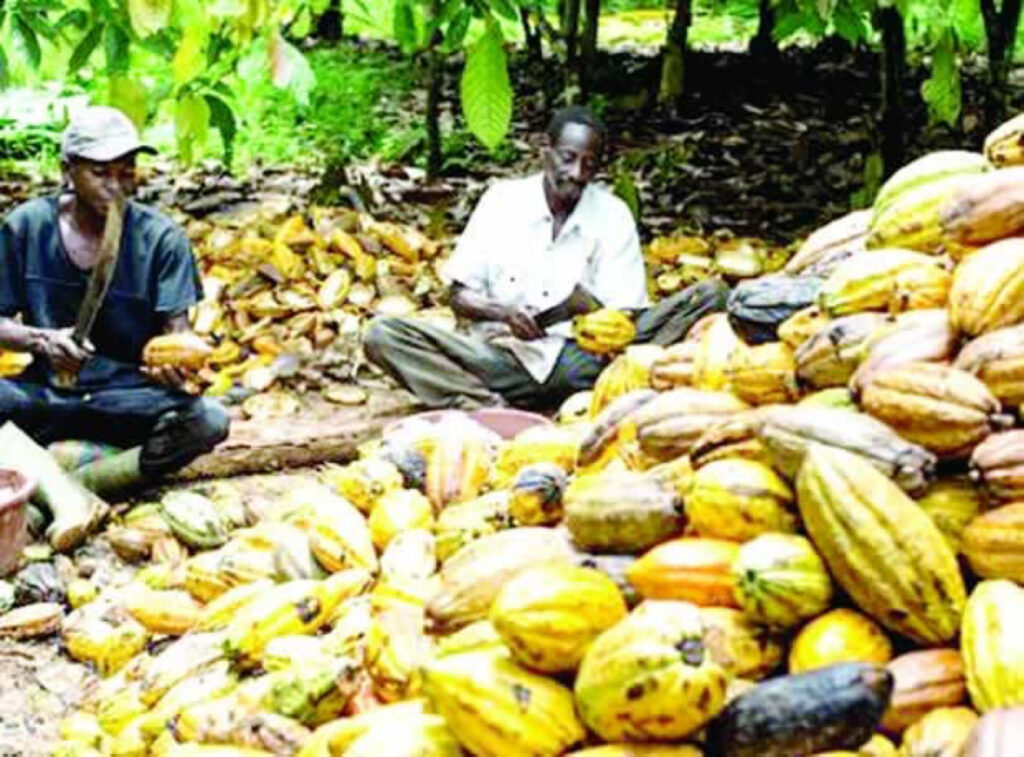

Dawn breaks gently over the cocoa heartlands of Ondo and Cross River. A low mist clings to the treetops, carrying with it the bittersweet aroma of freshly split pods. Farmers scoop the slick, pale beans into sacks soon to be claimed by local buying agents, the nerve centers of Nigeria’s cocoa trade.

LBAs are more than middlemen. Many operate with financing from processors or exporters, which means beans often have a predetermined destination before they are harvested. From rural aggregation points, they are trucked to warehouses or grinding plants, marking the beginning of the long journey from a Nigerian village to a European chocolate shelf.

According to the National Bureau of Statistics, Nigeria’s cocoa exports surged by 606 per cent in Q4 2024, from N171bn in Q4 2023 to about N1.2tn. Earlier in the year, exports had already climbed 304 per cent year-on-year to N438.7bn, fuelled by global demand, naira depreciation, and record prices following supply deficits in the Ivory Coast and Ghana.

But behind the numbers lies a sobering truth: the surge reflects price spikes, not higher production. Volumes remain flat, restrained by aging farms, poor roads, and insecurity. Without capital and reform, the sector risks missing its moment.

In 2024, cocoa prices broke 50-year records, soaring past $10,000 per metric tonne due to poor West African harvests, crop disease, and weather disruptions. The International Cocoa Organization estimated a global deficit of nearly 500,000 metric tonnes.

Even after easing, prices remain in the $7,000–$8,000 range, well above historical norms. Demand in Europe and North America barely softened, proving cocoa’s stubborn inelasticity.

For Nigerian farmers, this meant higher farmgate prices and rising rural incomes. For processors, however, expensive raw beans squeezed margins, with plants still running at just 30 per cent capacity. The boom revealed how fragile the sector is without deeper financing, modernization, and risk management.

Nigeria’s cocoa rests on tens of thousands of smallholders farming two to five hectares. To sell, they depend on LBAs, who are usually pre-financed by processors or exporters. This arrangement guarantees supply for financiers but limits farmers’ bargaining power and locks processors into costly short-term borrowing. Exporters, with access to offshore credit, often outcompete local processors.

The result is a financing cycle that devours working capital in bean procurement, leaving little room for plant upgrades, yield programs, or traceability. Even during high-price booms, structural progress remains elusive.

Real transformation depends not on the next rally, but on re-engineering finance. Controlling LBAs is crucial: processors must move beyond transactional ties to deeper integration, through estates, agronomy partnerships, or multi-year supply deals. Done right, this can double plant utilization, lift Earnings Before Interest, Taxes, Depreciation, and Amortization margins, and reduce volatility.

Modernization is equally urgent. Many Nigerian processing plants are outdated compared to automated grinders in Ghana, Côte d’Ivoire, and Asia. Digital traceability is the new frontier, as markets demand proof of sustainability. Far from a burden, traceability can command 5–7 per cent price premiums.

The financing model must be blended: long-term, low-cost development finance for infrastructure, paired with seasonal supply chain financing for procurement. Aligning capital to both horizons is key to building resilience.

Three regulatory forces are reshaping the market. First, the Living Income Differential, a $400-per-tonne premium, is designed to lift farmer incomes. Second, Nigeria’s National Cocoa Plan (2023–2032) targets yield improvement, governance, and traceability. Third, the EU Deforestation Regulation, effective late 2024, requires verifiable deforestation-free cocoa, with full supply chain mapping.

For unprepared operators, compliance will be costly. For well-capitalized players, it is a moat, securing access to premium markets and pushing weaker competitors aside. Regulation is no longer just compliance; it is a strategy.

Cocoa is also shifting in the eyes of investors. With export revenues in hard currency, it hedges against naira depreciation. Global scarcity and strong demand anchor high prices, while environmental, social, and governance compliance opens doors to sustainability-linked funds and green finance.

Certified cocoa, traceable to deforestation-free farms, sits at the sweet spot of profitability and impact. Coupled with Nigeria’s underutilized grinding plants, the investment case is strong: hard-currency cash flows, demand resilience, and sustainability premiums. Cocoa is no longer just an agricultural play; it is an emerging asset class.

Nigeria’s cocoa stands at a crossroads. Historic prices, new regulations, and global demand for sustainable supply have created a rare window. Yet, most of the crops still leave as unprocessed beans, forfeiting the value in grinding and branding.

Breaking the cycle demands patient, strategic capital: upstream integration, plant modernization, and traceability embedded across the chain. Investors who act now will secure yield, market share, and resilience while accessing the real wealth in the brown gold.